June 23, 2026—Today marks the release of Giving USA 2026: The Annual Report on Philanthropy, the most comprehensive and longest-running analysis of charitable giving in the United States. Produced by the Giving USA Foundation, a public service initiative of The Giving Institute, in partnership with the Indiana University Lilly Family School of Philanthropy, this report examines giving trends and philanthropic behavior across the country. Campbell & Company is proud to support the report as a long-standing member of The Giving Institute.

The newly released data offers a detailed look at giving from individuals, foundations, corporations, and bequests during calendar year 2025. As organizations across the nonprofit sector continue to respond to shifting economic conditions and evolving donor expectations, Giving USA remains an essential resource for understanding where philanthropy has been—and where it may be headed.

“This year’s growth—particularly in bequests—invites an interesting question for our sector: are we starting to see the great wealth transfer take shape in real time?” asks Kate Roosevelt, Campbell & Company Co-President. “We may not have the full answer yet, but it’s clear that the ways donors give are evolving alongside generational change.”

Total Charitable Giving:

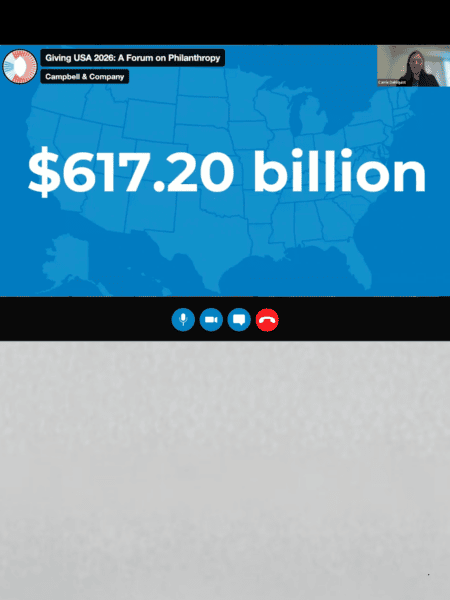

In 2025, total charitable giving in the United States reached $617.20 billion, representing a 5.7% increase over 2024 (3.0% when adjusted for inflation).

Giving by Source:

Giving by Recipient Sector:

How Giving Is Classified:

An important feature of Giving USA is that it distinguishes between the source of a gift and its ultimate use.

Donor-Advised Funds (DAFs):

Donor-advised funds (DAFs) are charitable giving accounts administered by sponsoring organizations such as community foundations or national financial institutions. Donors contribute assets to a DAF, receive an immediate tax benefit, and then recommend grants to nonprofit organizations over time.

In Giving USA, DAFs are reflected in different ways depending on how the gift flows. Contributions into a DAF are typically counted as individual giving, while grants out of a DAF are categorized based on the type of organization receiving the funds—for example, education, human services, or other subsectors.

This approach ensures that giving is tracked according to where it ultimately has impact, rather than the intermediary vehicle used to facilitate the gift.

Public-Society Benefit Organizations:

The public-society benefit subsector includes organizations that address broad civic, community, and societal needs. According to the National Taxonomy of Exempt Entities, this category includes:

Examples include organizations like United Way, Jewish Federations, and advocacy groups.

As nonprofits plan for the future, the findings from Giving USA 2026 reinforce the importance of diversified fundraising strategies, strong donor relationships, and adaptability in a changing landscape.

At Campbell & Company, we help nonprofits navigate these trends—strengthening major gift strategies, planning for long-term growth, and building deeper relationships with donors.

For a deeper look at the data and what it means for your organization, join our upcoming national webinar.

We’re ready to invest in your success. Are you?