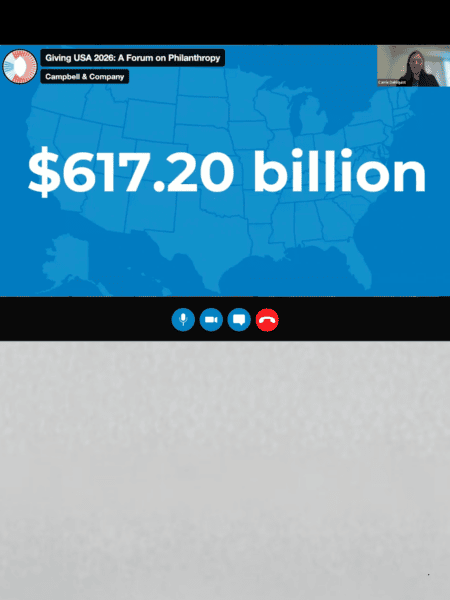

Thank you to everyone who joined us for the “Beyond the Report” webinar on October 16! We appreciated your engagement and the thoughtful questions submitted both in advance and during the live session.

As promised, we’re sharing responses to several additional questions we received outside of the live broadcast. These reflect the topics and concerns that are top-of-mind for nonprofit leaders and fundraisers as we navigate a rapidly changing philanthropic landscape. We hope these answers provide clarity and spark new ideas for your organization.

If you missed the session or would like to revisit the discussion, you can access the recording and slide deck here.

How does next year’s tax law change for everyday donors (under $2K) who don’t itemize help?

As we continue to unpack the One Big Beautiful Bill Act* (OBBBA)—now law as of July 2025—there are some key changes nonprofits need to understand. Beginning in 2026, the Universal Charitable Deduction allows taxpayers who don’t itemize to deduct up to $1,000 or $2,000 for charitable gifts. This could re-engage millions of small donors who previously got smaller and temporary tax benefits. Corporations also gain a bit of flexibility—they can now carry forward excess charitable deductions for five years. And starting in 2027, donors can receive a tax credit for gifts to qualifying scholarship-granting organizations. We encourage you to follow the National Council of Nonprofits’ website for the most up-to-date information on evolving policies and their implications.

*The One Big Beautiful Bill Act (OBBBA), officially designated Public Law 119-21, was signed into law on July 4, 2025. It originated as H.R. 1 in the 119th Congress.

What is considered a “highly compensated nonprofit employee”? Is it a set dollar amount or a relative amount to the organization’s budget?

Under OBBBA, the definition of a “highly compensated nonprofit employee” has been expanded for tax purposes. Previously, the excise tax on excess compensation applied only to the five highest-paid employees at a nonprofit who earned over $1 million in a given year. Starting in 2026, any employee at a tax-exempt organization who earns more than $1 million in total compensation (including salary, bonuses, deferred comp, and parachute payments) is now considered a “covered employee.” This triggers a 21% excise tax on the amount above $1 million, paid by the nonprofit employer.

Can a Qualified Charitable Distribution come out of a 401K or only an Individual Retirement Account?

QCDs may only be made from IRAs. However, an individual could consider transferring funds from their 401K to their IRA to make more funds available for a QCD.

Can a QCD be used to establish a Charitable Gift Annuity?

Yes, this is permissible due to changes introduced by the SECURE Act 2.0 in December 2022. Individuals 70 ½ or older may make a one-time $54,000 distribution from an IRA to create a CGA or other life income gift. The dollar limit is indexed to inflation and will grow slightly over time. Learn more.

How are DAFs treated under the new deductibility for individuals and families? Has the treatment of QCDs changed under the new regulations?

Gifts to DAFs are treated like any other charitable contribution for tax purposes. Regulation of QCDs is unchanged. However, they are not treated like itemized deductions, so they offer more opportunity for some donors who are now subject to the 0.5% “floor” and 35% cap for the highest earners. Learn more.

What are donor-advised fund entities doing to encourage more funding to DAFs, family funds, and then to distribute more generously?

We encourage you to check out the Giving USA Special Report – Donor Advised Funds: New Insights.

What will be the most significant changes for private foundations?

Private foundations will face a new tiered excise tax on net investment income, replacing the flat 1.39% rate with rates ranging from 2.78% to 10% depending on asset size. In addition to reduced grantmaking capacity, foundations will encounter more complex reporting requirements, stricter asset valuation rules, and expanded Form 990 disclosures. The 5% annual payout rule remains unchanged. Learn more.

How are trade policy changes impacting international donors?

Trade policy changes not only affect cross-border giving and donor confidence, but also have a direct impact on individuals’ financial resources at home. Shifts in tariffs, import/export regulations, and currency valuations can influence the broader economy, potentially reducing disposable income and the funds available for charitable donations. Nonprofits should closely monitor these regulatory and economic changes, as they may affect both international and domestic donor capacity. Read our recent blog: What Fundraisers Should be Watching.

Will legacy giving change in the current economic environment?

Factors that affect legacy giving (defined for our purposes here as giving through one’s estate plans) include federal and state estate tax exemptions, tax and estate planning generally (including whether someone does or does not have a will), charitable intent, and the degree to which people are invited by nonprofits they support to commit to a legacy gift such as a bequest intention. Changing economic conditions have little bearing on legacy giving other than the fact that some people are providing more financial support to children and grandchildren amid the effects of inflation and the cost of living.

Given the current uncertainty, how do we support donors in the gift-planning process?

Support donors by maintaining consistent, empathetic communication, offering flexible giving options, and reinforcing the long-term impact of their planned gifts. Transparency and reassurance are key during uncertain times!

What are the opportunities for successful Planned Giving in the current environment?

Over the next 20 to 25 years, the U.S. will experience the Great Wealth Transfer—a historic shift estimated up to $124 trillion from Baby Boomers to younger generations. Of that, $105 trillion is estimated to go directly to heirs, while $18 trillion is projected to be donated to charity. This moment presents a powerful opportunity for nonprofits to engage donors in legacy and planned giving conversations. As we look at donor behavior in this shifting financial landscape, one of the most important tools nonprofits should understand is the Qualified Charitable Distribution, or QCD.

Starting at age 73, individuals are required to take Required Minimum Distributions, or RMDs, from their retirement accounts—like IRAs and 401(k)s. These withdrawals are taxable. But here’s the opportunity: instead of taking the RMD and paying taxes, donors can choose to make a Qualified Charitable Distribution—up to $100,000 per year—directly to a nonprofit. This counts toward their RMD but is not taxed.

That’s a win-win. The donor reduces their taxable income, and the nonprofit receives a meaningful gift. It’s one of the most tax-efficient ways for older donors to give—and it’s underutilized.

Is there a concentration of DPI in the top income brackets, or is it distributed evenly across all households?

Great question—it is not evenly distributed.

What is the biggest change from last year to this year in the industry?

Nonprofit leaders cite financial instability, rising program demand, and workforce support as top concerns for 2025. There’s a shift toward strategic planning and adapting to uncertain funding landscapes. Read about the top concerns nonprofit leaders had entering 2025 here.

How will today’s policies impact the nonprofit sector moving forward?

Are donor priorities shifting in response to today’s unusual economic and political climate? The answer appears to be yes—but not in the same way we saw in 2016. Many donors are experiencing what’s being called ‘urgency fatigue’—a sense of burnout from constant crisis appeals. Instead of reacting with immediate giving, they’re becoming more selective, slower to commit, and focused on long-term impact. So, was the Trump bump a one-time phenomenon? Possibly. While some organizations may see renewed energy in 2025, the broader trend points to a need for reframing—moving from reactive appeals to strategic engagement that rebuilds donor energy and trust.

How can we tailor messaging for different donor segments?

Segmentation is more important than ever – to meet people where they are and tailor communications – and it requires a certain level of sophistication and spend in CRMs, etc. Research tools help you uncover donor insights using CRMs (like Raiser’s Edge and Salesforce), research engines (iWave, DonorSearch), AI (ChatGPT, Gemini), and platforms like Excel, LinkedIn, and Google.

We’d also be remiss not to mention the Giving by Generation report as a great resource for understanding how Gen Z, Millennials, Gen X, and Boomers each approach charitable giving. It highlights generational differences in giving amounts and preferences, volunteering habits, communication styles, and how technology and the COVID-19 pandemic have influenced donor behavior. Earlier this year, our Digital Donor Engagement team leveraged report findings to present “From Gen Z to Boomers,” linked here.

What are the most popular generational giving trends?

Younger donors favor mutual aid, crowdfunding, and noncash gifts like stocks. Donor-advised funds (DAFs) are growing across generations, while traditional cash donations are declining. Check out this update from the Urban Institute’s Giving Dashboard, which provides a snapshot of the many ways Americans give.

Should nonprofits expect more competition for foundation/corporation giving as a result of decreases/changes to federal funding?

We think it’s safe to say that the demand for philanthropic support, including grant funding, will grow in response to federal (and state) funding cuts.

For foundation and corporate giving, workforce development seems to be an emerging initiative. Please provide insight on this.

Workforce development has become a growing focus for foundations and corporate giving programs as funders seek to align social impact with business and community needs. This trend is driven by labor shortages, skill mismatches, and a desire to promote equitable economic mobility. Funders are shifting from one-off job training grants to long-term, partnership-based strategies that connect education providers, employers, and nonprofits to build sustainable career pathways. For more information, please check out The Urban Institute’s Local Workforce System Guide.

Do we feel that the trend of fewer donors but more money will continue, or can we keep and re-engage lapsed donors?

Don’t give up hope that this trend can be reversed. The Generosity Commission’s 2024 report offers smart and actionable recommendations for what we can do to engage and re-engage everyday givers across America.

What are the trends in giving to 1) early childhood development, 2) young children (0 to 5) with developmental delays, and international initiatives for global child development?

Trends in giving in these areas are hard to find and isolate from giving to education generally. However, the Early Childhood Funders Collaborative website includes a number of reports and resources on giving to early childhood education and development. In particular, there is a link to an Inside Philanthropy brief from 2022 (behind a paywall) on giving for early childhood education.

We encourage you to reach out if you’d like to chat more about these questions or discuss how current trends and policies are affecting your organization. Our team at Campbell & Company is always here to help you interpret the data, strategize for the future, and strengthen your fundraising efforts.

We’re ready to invest in your success. Are you?